TL;DR:

- Equity compensation in Century City executive contracts involves complex structures like stock options, RSUs, and restricted stock, each with different risks and tax implications.

- Understanding vesting schedules, acceleration clauses, and performance benchmarks is crucial, as they significantly impact long-term payouts and protection in changing scenarios.

Equity compensation can look like a straightforward bonus on paper, but the reality is far more complicated for executives navigating Century City’s competitive corporate landscape. A single clause buried in your contract can mean the difference between a life-changing payout and walking away with nothing. The pay story of Hudson Pacific CEO Victor Coleman illustrates this perfectly: his equity awards dropped from $22 million in 2024 to zero in 2025 because performance targets went unmet. That kind of volatility is not an outlier. It is the reality of executive compensation, and it is why every executive at the table deserves sharp legal awareness before signing anything.

Table of Contents

- What is equity compensation in Century City executive contracts?

- Key negotiations: Vesting, triggers, and acceleration terms

- Case study: When performance changes everything

- Protecting yourself: Legal rights and expert negotiation strategies

- Expert take: The equity details most executives overlook

- Protect your equity: Century City legal guidance for executives

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand equity types | Know the differences between stock options, RSUs, and restricted stock before negotiating. |

| Scrutinize vesting triggers | Whether your contract uses single- or double-trigger acceleration has huge payout implications. |

| Negotiate performance clauses | Demand clear and fair benchmarks to avoid losing your equity unexpectedly. |

| Get expert legal review | Independent counsel protects your interests and can strengthen your negotiation position. |

What is equity compensation in Century City executive contracts?

Century City sits at the intersection of entertainment, finance, real estate, and technology. Companies headquartered or operating here offer executive packages that go well beyond base salary. Equity compensation is the cornerstone of those packages, designed to align your long-term financial interests with the company’s growth. But not all equity is the same, and understanding what you are being offered matters enormously.

The three most common forms of equity compensation in Century City executive agreements are stock options, restricted stock units (RSUs), and restricted stock grants. Each carries different tax treatment, different risk profiles, and different vesting structures.

Stock options give you the right to purchase company shares at a set price, known as the strike price or exercise price, at a future date. If the stock price rises above that level, you profit on the difference. If it does not, the options expire worthless. Options are popular in startup environments and growth-stage companies where share prices are expected to appreciate.

Restricted stock units (RSUs) are promises to deliver actual company shares once certain conditions are met, typically time-based vesting. Unlike options, RSUs have value even if the stock price falls, because they represent real shares rather than the right to buy at a fixed price. RSUs are now the dominant form of equity in publicly traded companies.

Restricted stock involves an outright grant of company shares that vest over time and may be subject to forfeiture if you leave before the vesting period ends. This form is more common in private companies or with founders.

Equity vesting schedules in executive contracts typically run on a 4-year timeline with a 1-year cliff. That cliff means you receive nothing for the first 12 months, then a larger block vests on the first anniversary, followed by monthly or quarterly vesting for the remaining three years. This structure protects employers by encouraging retention, but it also means that leaving before year one results in zero equity earned.

| Equity type | Best suited for | Upside potential | Risk if stock declines |

|---|---|---|---|

| Stock options | Growth-stage companies | Very high | High (may expire worthless) |

| RSUs | Public companies | Moderate to high | Low (always have value) |

| Restricted stock | Private companies, founders | High | Moderate |

Executive packages in Century City almost always involve some combination of these instruments. Understanding how they interact with your base salary, bonus structure, and executive severance disputes is essential before you accept any offer. You should also pay close attention to how your equity intersects with any non-compete agreements in your contract, since leaving for a competitor could jeopardize unvested shares.

Key negotiations: Vesting, triggers, and acceleration terms

Now that equity types are clear, understand the negotiation details that powerfully affect your payout and security. The single most important negotiation beyond the size of your grant is what happens to unvested equity when things change suddenly, whether through a company sale, a merger, or an involuntary termination.

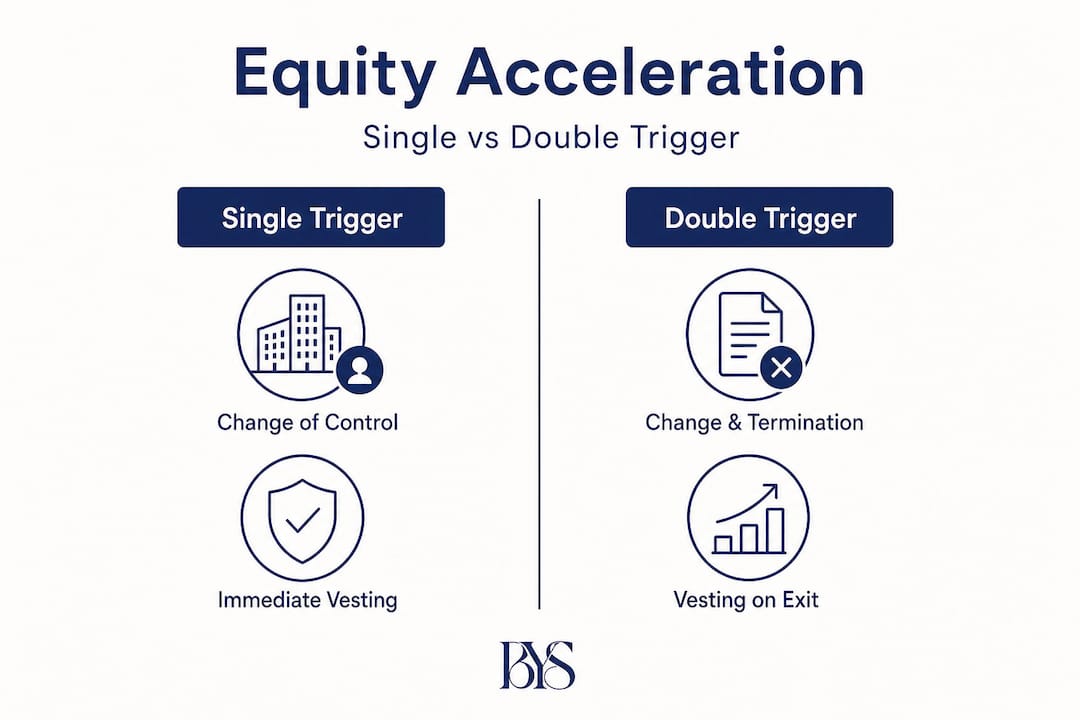

This is where acceleration clauses come in. These provisions determine whether your unvested equity speeds up and vests immediately under certain circumstances. There are two main structures, and they serve very different interests.

Single-trigger acceleration means your equity vests automatically upon a single event, typically a change of control such as a merger or acquisition. If the company is sold, you get your shares. This is strongly in your favor as an executive. You are not dependent on staying with the acquiring company or being fired by them to collect what you earned.

Double-trigger acceleration requires two events to occur before your equity vests: first, a change of control, and second, an involuntary termination or a material reduction in your role. Companies strongly prefer this approach because it gives the acquirer a reason to retain you. Executives and companies often clash sharply on this point, with employers pushing double-trigger for retention leverage and executives pushing for single-trigger or at minimum partial acceleration.

Pro Tip: Ask for partial acceleration even if full single-trigger is off the table. Partial acceleration on 50% of unvested shares upon a change of control is a common compromise that gives you meaningful protection while giving the acquirer some retention incentive.

Here is how these two structures compare in real scenarios:

| Scenario | Single-trigger outcome | Double-trigger outcome |

|---|---|---|

| Company is acquired, you stay | Full vesting | No acceleration |

| Company is acquired, you are laid off | Full vesting | Full acceleration |

| Company is acquired, your role is diminished | Full vesting | May trigger, depending on definition |

| No acquisition, you are terminated without cause | Depends on contract | Depends on contract |

Negotiating these terms requires you to think carefully about your executive termination rights and how your equity will be treated in a separation scenario. What counts as “involuntary termination” must be defined clearly in the agreement. Does it include constructive dismissal? What about a demotion or relocation? Vague language here is always resolved in the employer’s favor unless you push for specificity up front.

Other critical negotiation points include:

- Cliff duration. Can you negotiate the 1-year cliff down to 6 months? In competitive hiring markets, this is sometimes achievable.

- Vesting acceleration for cause definitions. Make sure “termination for cause” is narrowly and specifically defined so it cannot be used to strip your equity.

- Performance vesting conditions. If any portion of your equity is performance-based, the benchmarks must be objective, measurable, and fair.

- Exercise windows. If you hold options, how long do you have to exercise them after leaving? The standard 90 days is often too short. Push for 12 months or longer.

- Board discretion clauses. Watch for language that gives the board discretionary power to modify or cancel equity awards. This is a significant red flag.

Working with an independent legal advisor who specializes in executive employment agreements is not optional at this level. It is the single most effective step you can take to protect yourself.

Case study: When performance changes everything

To see why the fine print matters, let’s look at a high-profile performance case in Century City. Hudson Pacific Properties, headquartered in Century City, made national headlines in the executive compensation world when its CEO Victor Coleman saw his equity awards effectively disappear between 2024 and 2025.

In 2024, Coleman received equity awards valued at approximately $22 million. In 2025, those awards fell to zero. The reason: performance conditions embedded in the equity grants were not satisfied.

This is not a story about a failing company. It is a story about how performance-linked equity can completely redefine what an executive earns. The company’s board tied a significant portion of CEO compensation to metrics that, when unmet, resulted in a complete elimination of the equity award for that year. The dramatic swing in Coleman’s pay is a clear illustration of the stakes involved.

What this means for you: Performance-based equity is increasingly common in Century City executive packages, particularly in real estate, media, and financial services firms. These awards may be structured as performance share units (PSUs) or performance-leveraged RSUs where the number of shares you actually receive depends on hitting target metrics such as revenue growth, total shareholder return, or EBITDA thresholds.

The problem is that most executives spend their negotiation energy on grant size and vesting schedules, not on the fairness and clarity of performance benchmarks. That is a costly mistake.

Pro Tip: Insist on performance metrics that are within your sphere of influence. Company-wide revenue targets that depend on macro conditions outside your control are unfair measures for individual equity grants. Push for role-specific metrics or hybrid structures that include a time-based floor.

If you face a situation where your equity is retroactively denied or your contract is terminated in connection with performance disputes, understanding your wrongful termination rights in California becomes critical. California law provides strong protections, and performance-based terminations can sometimes mask discriminatory or retaliatory motives that an attorney can identify and challenge.

Protecting yourself: Legal rights and expert negotiation strategies

Performance issues highlight risk. Here is how to proactively safeguard your contract and compensation from day one. Protection starts before you sign, not after things go wrong.

Independent legal review is not just advisable, it is essential. Many executives assume that because a company uses “standard” agreements, there is little room to negotiate. That assumption consistently costs people money. Independent counsel for equity negotiations can identify clauses that look routine but carry serious financial consequences, and they can push back with authority.

Here are the most effective strategies for protecting your equity position:

- Benchmark your offer. Use compensation data from comparable companies and roles to establish whether your grant size, vesting schedule, and acceleration terms are genuinely competitive. Never accept the first offer as the ceiling.

- Negotiate in writing. Everything discussed verbally means nothing. Get all modifications to equity terms documented in the agreement or in binding written amendments before you start.

- Define all key terms. “Change of control,” “cause,” “good reason,” and “involuntary termination” must be defined specifically in your contract. Ambiguity is always a risk you carry.

- Understand the tax implications. The tax treatment of stock options (especially incentive stock options, or ISOs, versus non-qualified stock options, or NQSOs) is significantly different. RSUs are taxed as ordinary income upon vesting. These differences affect your real net compensation.

- Watch for discretionary override clauses. Any provision that allows the board or compensation committee to unilaterally reduce, delay, or cancel your equity without defined criteria is a clause worth fighting to remove or limit.

- Look at the equity plan documents. Your grant agreement is subordinate to the company’s equity plan. Read the plan itself, not just your individual grant letter.

California law offers meaningful protections that executives in other states do not have, including strong restrictions on non-competes and robust anti-discrimination statutes. If you believe your equity negotiation or compensation structure reflects gender discrimination in equity negotiations, California’s Fair Employment and Housing Act provides significant remedies.

Pro Tip: If you are negotiating as a woman or a person of color in a Century City firm, document the compensation benchmarks and the negotiation timeline carefully. Disparities in equity grants along gender or racial lines are legally actionable in California, and having documentation from the start strengthens any future claim.

Expert take: The equity details most executives overlook

Here is the perspective that most executives do not hear until it is too late: the biggest equity negotiation mistakes are not made by people who do not understand finance. They are made by people who do not understand leverage.

Most experienced executives entering a Century City role spend their energy on base salary and total grant value. Those are important, but they are also the easiest numbers to advertise and the hardest to move dramatically. The real value in executive compensation lives in the structural details: the acceleration terms, the definition of cause, the performance metric design, and the exercise window. These are the clauses that determine whether your equity actually converts into wealth.

There is a widespread assumption in executive hiring that every offer reflects “market standard” terms. That phrase is used strategically to discourage pushback. In reality, there is no single market standard for acceleration clauses, performance trigger definitions, or post-employment exercise periods. These terms vary significantly by company, sector, and negotiating sophistication. When you treat a company’s first offer as a benchmark, you are letting someone else define your worth.

The executives who come out ahead are those who approach the agreement as a legal document first and a compensation summary second. They bring in counsel early, they ask the uncomfortable questions about what happens when things go wrong, and they push for contract language that protects them in scenarios that feel hypothetical on signing day but become very real on termination day. Our expert legal strategies page outlines the kinds of disputes that arise when these details are left unresolved.

The equity in your executive contract is not a gift. It is compensation you earn. Treat it with the same seriousness you would apply to any other financial asset, and protect it accordingly.

Protect your equity: Century City legal guidance for executives

Navigating executive equity compensation requires more than financial acumen. It requires legal precision. Shirazi Law Office works with executives and senior management across Century City to review, negotiate, and protect employment contracts at the highest level. Whether you are entering a new agreement, facing a dispute over unvested equity, or dealing with a termination that puts your awards at risk, personalized legal guidance can make all the difference. Explore the firm’s approach to Century City executive dispute advice and learn how specialized executive legal representation can protect your long-term compensation and professional future.

Frequently asked questions

What are the most common forms of equity compensation for executives in Century City?

Stock options, RSUs, and restricted stock with 4-year vesting and a 1-year cliff are the most prevalent structures in Century City executive agreements.

Is single-trigger or double-trigger acceleration better for executives?

Single-trigger acceleration offers more security for executives because it pays out upon a change of control alone, while double-trigger requires both a sale and an involuntary termination, making independent legal counsel essential when negotiating this provision.

Can equity awards be reduced or canceled based on performance?

Yes, and the stakes are significant: Hudson Pacific’s CEO saw equity awards drop from $22 million to zero in a single year due to unmet performance conditions, highlighting how critical clear and fair performance benchmarks are in any executive agreement.

Should I hire a lawyer to negotiate my executive equity package?

Independent counsel is strongly recommended because double-trigger and single-trigger provisions, performance clauses, and cause definitions carry significant financial consequences that require legal expertise to identify and address before you sign.

Recommended

- Executive disputes at Century City firms: A practical guide – Law Office of Brian Y. Shirazi, PC

- Non-Compete Agreements: Executive Mobility in Century City

- Century City Gender Discrimination In Private Equity: 2026 – Law Office of Brian Y. Shirazi, PC

- Executive Severance Disputes Impact Century City Leaders